AML Regulations for Real Estate and DNFBPs in the UAE – 10 Updated Rules & Guidelines 2026

Anti-Money Laundering (AML) regulations in the UAE have become stricter in 2026. The government has strengthened its legal framework to align with global standards and prevent financial crimes. Real estate businesses and Designated Non-Financial Businesses and Professions (DNFBPs) now face higher compliance expectations, stricter monitoring, and heavier penalties.

Real estate is a high-risk sector. It involves large transactions, cross-border investors, and complex ownership structures. That is why UAE regulators closely monitor it.

This guide explains 10 updated AML rules for 2026. It also highlights key actions businesses must take to stay compliant.

1. Federal AML Law Applies to Real Estate and DNFBPs

The UAE AML framework is based on Federal Decree-Law No. 20 of 2018, now strengthened by the 2025 AML Law updates.

The UAE AML framework is based on Federal Decree-Law No. 20 of 2018, which serves as the primary legislation governing anti-money laundering and counter-terrorism financing in the country.

Under this law and its implementing regulations, real estate brokers, agents, and developers are classified as Designated Non-Financial Businesses and Professions (DNFBPs) and are subject to full AML obligations.

The law explicitly requires DNFBPs to apply customer due diligence, risk assessment, and record-keeping measures—placing them within the same regulatory framework as financial institutions.

Key Takeaway:

You cannot treat AML as optional

Small firms are also fully regulated

| Section | Law / Regulation | Quoted Source | Key Explanation |

|---|---|---|---|

| Legal Basis of UAE AML Framework | Federal Decree-Law No. 20 of 2018 on AML/CFT | “The primary legislation governing AML in the UAE is Federal Decree-Law No. 20 of 2018…” | This law forms the core AML framework in the UAE and applies to both financial and non-financial sectors. |

| DNFBPs Covered Under AML Law |

Federal Decree-Law No. 20 of 2018 Cabinet Decision No. 10 of 2019 |

“Real estate brokers and agents are classified as designated non-financial businesses and professions (DNFBPs) and are therefore subject to full AML obligations.” | Real estate businesses fall under DNFBPs and must comply with AML regulations. |

| DNFBPs Same as Banks | Cabinet Decision No. 10 of 2019 | “Designated non-financial businesses and professions… include real-estate agents… and are within the same regulatory perimeter as banks.” | DNFBPs follow similar AML compliance obligations as financial institutions. |

| AML Obligations Apply Equally | Federal Decree-Law No. 20 of 2018 (Article 16) | “Financial institutions and designated nonfinancial businesses and professions shall… identify risks… apply due diligence… and maintain records.” | Both DNFBPs and financial institutions must apply CDD, risk assessment, and record-keeping. |

| Real Estate Sector Under AML Scope | UAE AML Regulatory Guidance | “All DNFBPs and particularly the real estate agents and brokers are now subject to the AML law in the UAE.” | Real estate agents and brokers are explicitly regulated under UAE AML laws. |

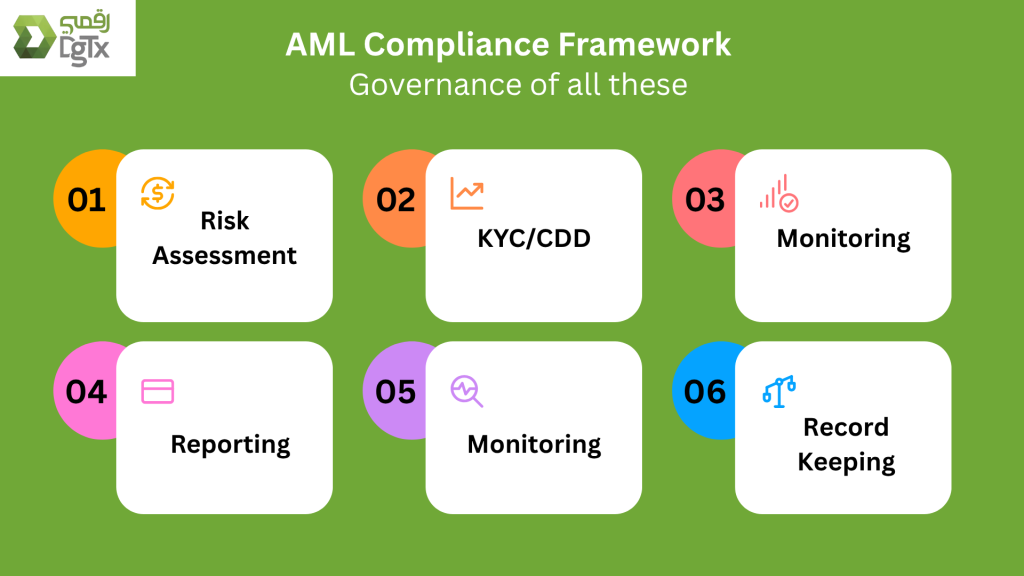

2. Mandatory Risk-Based Approach

Businesses must identify and assess risks before dealing with clients.

This includes:

Customer risk (high-net-worth, foreign buyers)

Geographic risk (high-risk countries)

Transaction risk (cash deals, unusual patterns)

A risk-based approach helps firms apply stronger controls where needed.

infographics

Low Risk → Simplified Checks

These are clients or transactions that are unlikely to involve money laundering or fraud.

What you do:

Basic identity verification (ID/passport)

Minimal documentation

Less frequent monitoring

Medium Risk → Standard Checks

These cases have some risk factors, so you follow normal due diligence procedures.

What you do:

Full KYC (Know Your Customer)

Verify source of funds

Regular monitoring of transactions

High Risk → Enhanced Due Diligence (EDD)

These clients or transactions have a higher chance of financial crime, so stricter checks are required.

What you do:

Detailed source of wealth and funds verification

Background checks

Ongoing and frequent monitoring

Senior management approval

| Risk Type | What It Means | Key Risk Indicators | Example | Why It Matters |

|---|---|---|---|---|

| Customer Risk | Risk based on the identity and background of the client |

- High-net-worth individuals (HNWIs) - Foreign buyers - Politically Exposed Persons (PEPs) - Complex ownership structures |

A foreign investor buys a luxury property using an offshore company registered in a tax haven | May indicate hidden ownership or unclear source of funds used to launder money |

| Geographic Risk | Risk based on the country of origin of the client or funds |

- Clients from high-risk or sanctioned countries - Weak AML jurisdictions - FATF grey-listed countries |

A buyer from a high-risk country invests in multiple properties and pushes for quick transactions | Funds may be linked to money laundering or terrorist financing activities |

| Transaction Risk | Risk based on how the transaction is structured or executed |

- Large cash payments - Third-party payments - Over/under-valued property deals - Rapid buying and selling (flipping) |

A buyer pays partly in cash and uses multiple third-party accounts for the remaining amount | Complex transactions may be used to disguise the origin of illegal funds |

3. Customer Due Diligence (CDD) is Compulsory

Customer Due Diligence (CDD) requires you to verify a client’s identity, business details, and transaction purpose before starting any relationship to prevent fraud and ensure AML compliance, while Ultimate Beneficial Owner (UBO) identification helps you find the real individual who ultimately owns or controls a business, even if hidden behind complex structures; this process plays a critical role for DNFBPs and real estate sectors as it reduces money laundering risks, ensures regulatory compliance, and protects businesses from penalties while strengthening transparency and trust.

You must verify every client before starting a business relationship.

CDD includes:

Identity verification (passport, Emirates ID)

Business verification (for companies)

Understanding purpose of transaction

Identifying Ultimate Beneficial Owner (UBO)

Key Takeaways

Never accept anonymous or incomplete client information.

4. Enhanced Due Diligence (EDD) for High-Risk Clients

Enhanced Due Diligence (EDD) means you perform deeper checks on high-risk clients to understand their identity and source of funds. In the United Arab Emirates, businesses use EDD to meet strict AML laws and protect the financial system. Regulators enforce stricter rules to stop money laundering, terrorism financing, and hidden ownership structures.

EDD applies to:

Politically Exposed Persons (PEPs)

High-value property transactions

Clients from high-risk jurisdictions

The new regulations expand the definition of PEPs and require deeper checks.

What to Do:

Verify source of funds

Conduct background checks

Increase monitoring frequency

| Action | How It Can Be Done | Process | Time Required |

|---|---|---|---|

| Verify Source of Funds | Collect bank statements, salary slips, contracts, or sale agreements | Review documents, match income with transaction value, check consistency | 1–3 business days |

| Conduct Background Checks | Use AML screening tools, sanctions lists, and public records | Screen client against PEP/sanctions lists, review legal history and risk indicators | Same day – 2 days |

| Increase Monitoring | Set up automated alerts and periodic reviews | Monitor transactions regularly, flag unusual activity, update risk profile if needed | Ongoing (daily/monthly reviews) |

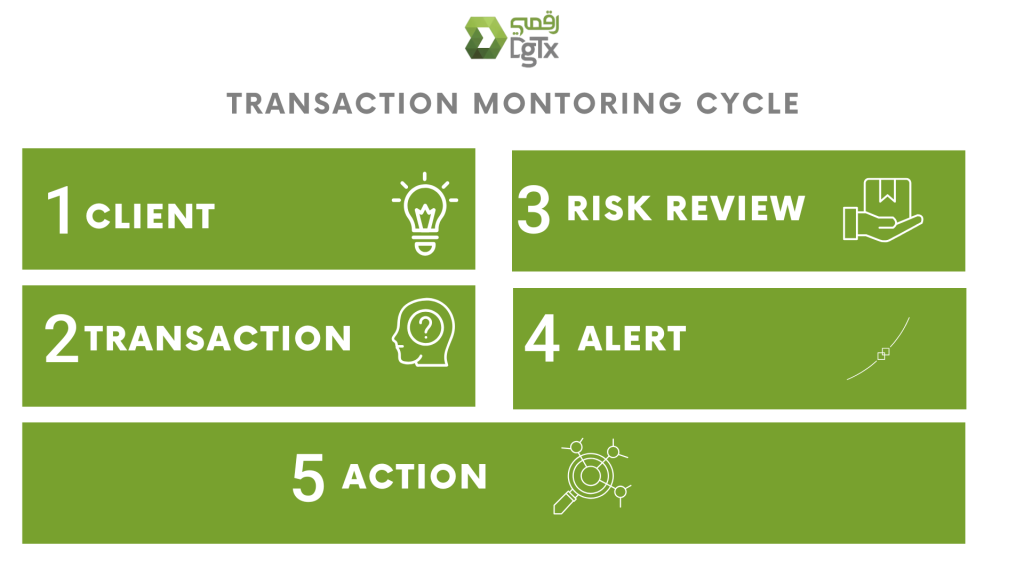

5. Ongoing Transaction Monitoring is Required

AML compliance is not a one-time process. You must continuously monitor transactions.

Suspicious indicators include:

Large cash payments

Property overvaluation or undervaluation

Complex ownership structures

These are common red flags in real estate laundering cases.

6. Mandatory Reporting via goAML

All DNFBPs must report suspicious transactions using the goAML system.

Reports include:

STR (Suspicious Transaction Report)

REAR (Real Estate Activity Report)

Failure to report can result in heavy penalties.

Real estate firms must report large or suspicious transactions promptly.

7. Record Keeping for Minimum 5 Years

Businesses must maintain records of:

Customer data

Transaction history

Due diligence documents

The law requires records to be kept for at least 5 years.

Why it Matters:

Helps audits and investigations

Protects your business from penalties

8. Appointment of Compliance Officer

Every DNFBP must appoint a qualified AML compliance officer.

Responsibilities include:

Monitor compliance

Report suspicious activities

Train staff

New regulations emphasize stronger governance and accountability.

9. Internal Policies, Controls, and Training

Businesses must create a complete AML program.

This includes:

Written AML policies

Internal controls

Employee training

Regular audits

Continuous staff training is critical to detect risks early.

Infographic:

AML Program Structure:

Policies → Controls → Training → Audit → Improvement

10. Increased Penalties and Regulatory Inspections

The UAE has increased enforcement actions in 2026.

Millions in fines imposed on DNFBPs

Real estate firms heavily targeted

Regular inspections by authorities

Authorities now focus on actual implementation, not just documentation.

Key Warning:

Non-compliance can lead to:

Heavy fines

Business suspension

Legal action

Real Estate AML Risk Areas (Infographic)

HIGH-RISK SCENARIOS:

✔ Cash property purchases

✔ Rapid buying & selling

✔ Third-party payments

✔ Offshore ownership

✔ PEP involvement

Key Points to Consider for 2026

✅ 1. Compliance is No Longer Optional

Authorities are strict. Even small firms face inspections.

✅ 2. Technology is Essential

Use AML software for:

Screening

Monitoring

✅ 3. Documentation is Critical

If it is not documented, it is considered non-compliant.

✅ 4. Focus on UBO Transparency

Authorities want to know the real owner behind every transaction.

✅ 5. Be Ready for FATF Evaluation

The UAE is under global monitoring. Compliance standards are rising.

Practical Compliance Checklist

✔ Register on goAML

✔ Conduct risk assessment

✔ Implement KYC/CDD process

✔ Monitor transactions

✔ Report suspicious activity

✔ Maintain records

✔ Train staff regularly

✔ Appoint compliance officer

✔ Conduct internal audits

✔ Update policies annually

Conclusion

AML Regulations for DNFBPs and Real Estate in the UAE have evolved significantly in 2026. The government has introduced stricter laws, enhanced monitoring, and stronger enforcement.

Real estate businesses must act now. They must implement a complete AML framework, train their teams, and ensure full compliance.

Ignoring AML is no longer an option. It can damage your reputation, lead to fines, and even shut down your business.

👉 The smart approach is simple:

Build strong compliance today to avoid risk tomorrow.

AML Regulations UAE – FAQs

What are AML regulations for real estate and DNFBPs in the UAE?

AML regulations for real estate and DNFBPs in the UAE require businesses to verify customers, monitor transactions, report suspicious activities, and maintain records to prevent money laundering and terrorist financing.

Who falls under DNFBPs in the UAE?

DNFBPs include real estate agents, brokers, dealers in precious metals and stones, auditors, accountants, and corporate service providers operating in the UAE.

Is AML compliance mandatory for real estate companies in the UAE?

Yes. AML compliance is mandatory for all real estate businesses in the UAE. Authorities require firms to follow strict regulations and report suspicious transactions through the goAML system.

What is Customer Due Diligence (CDD) in UAE AML regulations?

Customer Due Diligence (CDD) is the process of verifying a client’s identity, understanding the nature of the transaction, and identifying the ultimate beneficial owner before starting a business relationship.

When is Enhanced Due Diligence (EDD) required in the UAE?

EDD is required when dealing with high-risk clients such as politically exposed persons (PEPs), clients from high-risk countries, or large and complex real estate transactions.

What is goAML and why is it important?

goAML is an online reporting system used in the UAE to submit suspicious transaction reports (STRs) and real estate activity reports. It is mandatory for DNFBPs to register and report through this system.

What are the penalties for non-compliance with AML regulations in the UAE?

Penalties include heavy fines, business suspension, license cancellation, and legal action. Authorities have increased enforcement in 2026.

How long should AML records be kept in the UAE?

Businesses must keep AML records, including customer data and transaction details, for at least five years as per UAE regulations.

What are common AML risks in the UAE real estate sector?

Common risks include large cash transactions, use of third parties, offshore ownership structures, and rapid buying and selling of properties.

Do small real estate businesses need to follow AML regulations in the UAE?

Yes. AML regulations apply to all businesses, regardless of size. Small firms must implement the same compliance measures as large companies.